Crash on Route 202 in Jaffrey leads to trapped driver, fuel spill

Crash on Route 202 in Jaffrey leads to trapped driver, fuel spill

Bernie Watson of Bernie & Louise dies at 80

Bernie Watson of Bernie & Louise dies at 80

‘The Last Laugh’ coming to Town Hall Theatre in Wilton

‘The Last Laugh’ coming to Town Hall Theatre in Wilton

Echoes of Floyd performs Saturday at Peterborough Town House

Echoes of Floyd performs Saturday at Peterborough Town House

End Sexual Violence on Campus group holding April 27 event

End Sexual Violence on Campus group holding April 27 event

Hancock Town Library schedules paper sculpture workshop

Hancock Town Library schedules paper sculpture workshop

Children and the Arts Festival in Peterborough will have bird theme

Children and the Arts Festival in Peterborough will have bird theme

Cosy Sheridan speaks and performs for Monadnock Writers’ Group

Singer-songwriter Cosy Sheridan of Harrisville spoke and performed for the Monadnock Writers’ Group Saturday in honor of National Poetry Month.After talking about her songwriting process, Sheridan led the group in a free writing exercise, followed by...

Mountain Shadows School hosts Olympic Studies Night

According to Temple Brighton, one of the co-founders of Mountain Shadows School, the school’s Olympic Studies Night was inspired by the 1984 Summer Olympics in Los Angeles. “There was so much energy around those Olympics, and all this excitement, and...

Most Read

BUSINESS QUARTERLY – New housing projects could provide relief

BUSINESS QUARTERLY – New housing projects could provide relief

Yoko Ono to receive MacDowell Medal

Yoko Ono to receive MacDowell Medal

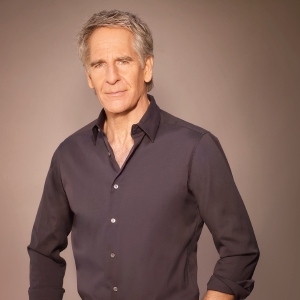

Scott Bakula starring in Peterborough Players’ ‘Man of La Mancha’

Scott Bakula starring in Peterborough Players’ ‘Man of La Mancha’

Mountain Shadows School hosts Olympic Studies Night

Mountain Shadows School hosts Olympic Studies Night

HOMETOWN HEROES – Rose Novotny is motivated by community

HOMETOWN HEROES – Rose Novotny is motivated by community

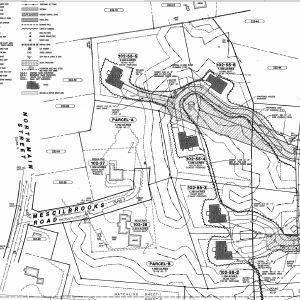

BUSINESS QUARTERLY – Antrim Planning Board approves Battaglia subdivision

BUSINESS QUARTERLY – Antrim Planning Board approves Battaglia subdivision

Editors Picks

HOUSE AND HOME: The Old Parsonage in Antrim is a ‘happy house’

HOUSE AND HOME: The Old Parsonage in Antrim is a ‘happy house’

Former home of The Folkway in Peterborough is on the market

Former home of The Folkway in Peterborough is on the market

Two Jaffrey-Rindge Destination Imagination teams move on to Globals

Two Jaffrey-Rindge Destination Imagination teams move on to Globals

Old Homestead Farm in New Ipswich requests variance for short-term rental cabins

Old Homestead Farm in New Ipswich requests variance for short-term rental cabins

Sports

Katalina Davis dazzles in Mascenic shutout win

The Mascenic softball team soared to a 7-0 shutout win over regional and interdivisional rival Conant thanks to a dazzling performance on both sides of the ball from senior pitcher Katalina Davis. “When Kat’s on, they’re not hitting, so she was...

LOCAL SPORTS ROUNDUP: Conant girls’ tennis gets first win

LOCAL SPORTS ROUNDUP: Conant girls’ tennis gets first win

Conant girls’ tennis continues to seek improvement

Conant girls’ tennis continues to seek improvement

Jack Kidd and Kidd Gloves make donation to Mt. Monadnock Little League

Jack Kidd and Kidd Gloves make donation to Mt. Monadnock Little League

HIGH SCHOOL SPORTS ROUNDUP: Tasha MacNeil leads the way for ConVal at Pelham Invita

HIGH SCHOOL SPORTS ROUNDUP: Tasha MacNeil leads the way for ConVal at Pelham InvitaOpinion

Viewpoint: State Rep. Molly Howard – Public schools are the bedrock of communities

A recent Google search informed me that New Hampshire students rank sixth in the nation, according to U.S. News and World Report, with similar results on other sites.That’s pretty good, considering New Hampshire ranks 50th in public school funding,...

Business

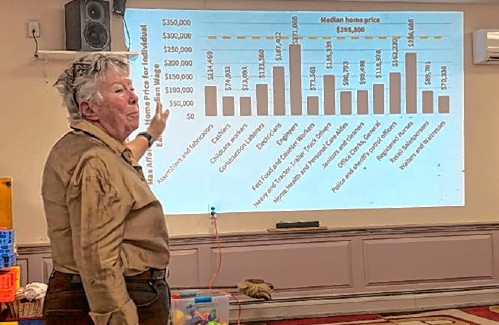

BUSINESS QUARTERLY: Grants allow towns to study housing

In 2022 the State of New Hampshire, in recognition of the housing shortage in the state, created a grant program to fund work in towns that wished to explore the housing situation in their town and consider ways to increase housing availability and...

BUSINESS QUARTERLY: Dan Petrone – A guide to the commission settlement

BUSINESS QUARTERLY: Dan Petrone – A guide to the commission settlement

BUSINESS QUARTERLY – New housing projects could provide relief

BUSINESS QUARTERLY – New housing projects could provide relief

BUSINESS QUARTERLY – Antrim Planning Board approves Battaglia subdivision

BUSINESS QUARTERLY – Antrim Planning Board approves Battaglia subdivision

e-Edition

Arts & Life

Yoko Ono to receive MacDowell Medal

Artist and activist Yoko Ono is this year’s recipient of the Edward MacDowell Medal. Ono, whose career as an artist began in the downtown New York scene in the early 1960s and has continued across seven decades, has developed a body of work...

Gnome Notes: Emerson Sistare – Amor Towles weaves tapestry in ‘Table for Two: Fictions’

Gnome Notes: Emerson Sistare – Amor Towles weaves tapestry in ‘Table for Two: Fictions’

Jaffrey Civic Center hosting Heart of the Arts

Jaffrey Civic Center hosting Heart of the Arts

Project Shakespeare to present ‘The Miraculous Journey of Edward Tulane’

Project Shakespeare to present ‘The Miraculous Journey of Edward Tulane’

The Thing in the Spring returns May 16

The Thing in the Spring returns May 16

Obituaries

Kevvin W. Sawtelle 31

Kevvin W. Sawtelle 31

Kevvin W. Sawtelle, 31 Jaffrey, NH - Kevvin W. Sawtelle, 31, of Rindge, died peacefully on April 5, 2024, in the arms of his family at the Dartmouth-Hitchcock Medical Center in Lebanon, NH after a long battle with brain cancer. Kevvin w... remainder of obit for Kevvin W. Sawtelle 31

Constance Boldini

Constance Boldini

Westmoreland, NH - Constance Marie (Wilson) Boldini, died April 16, 2024. She is predeceased by her husband Guido Boldini and her son Peter Vaillancourt. She is survived by two daughters, Anne Young of Tennessee, Brenda Bryer of Stoddar... remainder of obit for Constance Boldini

Beverly R. Gienty

Peterborough, NH - Beverly R. Gienty, 88, of Windsor, CT, formerly of Peterborough, Dublin, Francestown, and Jaffery NH passed away on April 14, 2024, at Kimberly Hall South, Windsor, CT. She was the widow of Edward H. Gienty. Beverly w... remainder of obit for Beverly R. Gienty

David Albin Shaw

David Albin Shaw

Peterborough NH - David A. Shaw, age 85, of Peterborough died April 7, 2024 after a long co-existence with Alzheimer's disease. He will be missed by his family, friends and devoted caregivers. His care and their love in the Memory Suppo... remainder of obit for David Albin Shaw